Facebook

Facebook

Twitter

Twitter

Pinterest

Pinterest

Copy Link

Copy Link

Coldwell Banker at Inman Connect San Francisco 2017

Inman Connect San Francisco brings together more than 4,000 of the most important people in real estate including top-producing agents and brokers, CEOs of leading real estate franchises and tech entrepreneurs to embrace and leverage the change that surrounds real estate.

Coldwell Banker showed up big this year. From the stage to the lobby Gen Blue was seen and heard – reminding the industry why it is real estate’s most iconic brand.

Below are some highlights from the week.

The President and CEO of Coldwell Banker, Charlie Young, gave an inspiring keynote from mainstage about how the Empowered Agent is bringing positive disruption to real estate and is a force to be reckoned with.

Charlie also wrote a piece for Inman on how to identify, embrace and support these talented specialists as we look to the future.

A special group of empowered agents were highlighted on mainstage including Team Diva with Coldwell Banker Bain in Seattle. Pictured on-screen below is Kim V. Colaprete and Roy Powell.

Lindsay Listanski, Senior Manager Media Engagement for Coldwell Banker, ran a social media crash course on how to implement geographic marketing using Facebook, Instagram and YouTube.

The audience ate it up and so did Inman. Lindsay’s presentation was packed full of how-tos, best practices and helpful tips on how to take your social media marketing to the next level and wow your sellers. You can catch her full presentation here.

David Marine, Senior Vice President of Marketing, predicted the future of real estate marketing. Spoiler alert: the future is video. He covered everything from local television advertising to how to effectively use video to bolster your listings. He also addressed how real estate brands should think about using tools like Zillow and Trulia to their advantage.

Coldwell Banker rounded out the week with a visit to the Nest Headquarters in Palo Alto.

Agents and brokers heard from Nest CMO Doug Sweeny about the future of the connected home and received a preview of what Nest is doing to support real estate Smart Home specialists.

Come back to CB Exchange for a new suite of marketing assets next month!

The networking and fun continued at the invite-only Coldwell Banker cocktail party – Smart Cocktails and Smart Conversations.

Even if you weren’t there in person you can catch up on everything you missed right here:

- David Marine on Why You Should Consider Advertising on Local TV

- David Marine on Zillow and Trulia

- Sam DeBrod on Why Brokerages Still Matter

- Terri King on the Value of a Franchise Brokerage and Coaching Your Team

- Charlie Young on Mainstage: The Empowered Agent

- Lindsay Listanski on Geographic Marketing using Facebook, Instagram and YouTube

Coldwell Banker sales associates can also stay in the know with Gen Blue News. Now available on Amazon Alexa, just enable Gen Blue News on your Amazon Echo or Echo Dot and say “”Alexa, Open Gen Blue News” or download the podcast through iTunes.

And if you’re still having FOMO make sure to join us at Gen Blue and Inman Connect NYC!

How to Prepare Your Home Before Going on Vacation

Ahhhhh, that summer vacation is on your radar now…just a few loose ends to wrap up before you hit the road!

Your summer vacation is finally here! You’ve booked flights, reserved hotel rooms, and scoped out the best places to eat along the way, but have you prepared your home for your absence?

Nothing spoils a vacation like returning to smelly trash, sad houseplants, or an unexpected break-in. Whether you plan to be gone for a week or a month, there are a few simple steps you can take to get your home ready so you can relax and enjoy your time away.

Clean Up

Leave your home exactly as you’d like to find it when you return—like new!

- Empty your refrigerator of any perishable foods that will pass their enjoy-by dates while you are away, and toss open pantry items that will mold or go stale.

- Take out the trash and recycling. Don’t forget about smaller trash cans in bathrooms and utility rooms.

- Finish, fold, and put away laundry. You’ll likely have clothes to wash when you return, so get a jumpstart before you go.

- Wash your sheets and towels, and remake your beds. You’ll thank your past self when you come home to fresh linens in clean bedrooms and bathrooms.

- Wipe down counters, run your garbage disposal, sanitize toilets, and organize clutter.

Close Out

Reduce the possibility of surprise maintenance issues, which can be costly to fix, by keeping up with regular home repairs throughout the year.

- Perform routine inspections and weatherize. Make sure your heating and cooling systems, gas and water lines, and roof and windows are in good shape. Clean up your yard, mow the grass, and take care of any dead trees or overhanging limbs that could cause damage in severe weather.

- Unplug all small appliances. This will save power and eliminate the potential for things to short-circuit and cause significant electrical damage.

- Check your smoke detectors. Batteries die, parts wear out, and dust and other pollutants can impede alarm performance. Make sure your home is prepared in case of fire, and consider integrating your detectors into your home security system so the fire department is notified in an emergency.

- Turn off your water at the main shut-off valve to prevent damage in the case of a burst pipe or water heater malfunction. Consider installing a water and flood sensor, which detects moisture where it shouldn’t be and pushes notifications to your smartphone.

- Leave your closet doors ajar to prevent mold and musty smells from building up.

Secure

Protect your home and belongings from thieves. The highest percentage of burglaries occur during the summer months, and homes without security or alarm systems are up to 300 percent more likely to be broken into.

- Set up remote monitoring. You can have a security system professionally installed or start with a wireless security camera that you can view from your smartphone. If you have a security monitoring service, let them know that you are traveling.

- Collect spare keys. If you have house keys hiding under doormats or flower pots, bring them inside so prowlers don’t find them. Leave an extra set with a trusted neighbor or friend in case there’s an issue that needs to be addressed while you’re away.

- Hold your mail and newspapers. Nothing signals that you are out of town like an overflowing mailbox or stack of unread papers on your front porch. Placing a hold with USPS is as easy as completing an online form and will prevent identity thieves from targeting sensitive information found in bills and credit card statements.

- Take advantage of home automation. You can link everything from smart locks that you can triple-check via smartphone app to smart doorbell cameras that sense motion on your front porch and have two-way audio.

- Close blinds into rooms that contain expensive items, and set up smart light timers that mirror your regular habits when you’re home.

- Ask for help. Have a neighbor park in your driveway while you’re gone, and enlist a friend to water your plants and check up periodically on your property.

A little bit of preparation will go a long way when it comes to leaving your home clean and secure, and enjoying your vacation stress-free!

Source: RisMedia

Light in, Prying Eyes out: Benefits of Light-Filtering Window Shades

Light and airy rooms but still worried about people sharing your indoor privacy? Then this is the read for you!

Want to let light in while keeping your nosy neighbors out? Special types of light-filtering window treatments enable you to illuminate your home with natural light while preventing others from viewing your personal space. Ultimately, these window shades may prove to be exceedingly valuable, particularly for homeowners who are searching for high-quality window treatments that are both stylish and practical.

Benefits

In addition to offering maximum privacy from passersby and neighbors, light-filtering window shades provide many benefits, including:

Energy Savings: The U.S. Department of Energy points out properly installed window shades offer some of the “simplest, most effective window treatments for saving energy.”

Improved Insulation: Some light-filtering window shades have been shown to act as both insulation and air barriers, and control air infiltration more effectively than other types of window treatments.

Exceptional Value: Homeowners can enjoy light-filtering window shades that consist of UV-resistant and antimicrobial materials for superb quality, maintaining their value over time.

Eco-Friendly Styles: Some light-filtering window shade options are partly constructed from biodegradable materials.

Unparalleled Convenience: Light-filtering window treatments can be motorized or manual, allowing for ease of use both day and night.

Types of Light-Filtering Window Shades

Light-filtering window shades provide varying degrees of light infiltration. The most popular options include:

Cellular Shades

Cellular shades deliver year-round insulation and privacy. Meanwhile, they are constructed to allow small amounts of light to enter a room. Typically, cellular shades are sold in single or double thickness. They are available in multiple vibrant colors, along with various cell sizes and fabric styles to match your home decor.

Cellular shades also boast immense durability. They include an aluminum headrail and bottomrail and take only minutes to set up in any living space.

Roller Shades

Roller shades are easy to use and come in a wide range of lifts to complement any home’s decor. Light-filtering roller shades are top choices for many homeowners, as these shades block visibility into your personal space. In addition, blackout roller shades are great choices for those who prefer extra privacy and will help you maximize light control consistently.

Roman Shades

For those who want to add a hint of luxury to th eir decor, there may be no better option than Roman shades. Top-down/bottom-up Roman shades allow you to control whether light will enter from the bottom or from above. The versatile options in fabric range from every color of the rainbow, as well as prints.

If you require additional privacy, select Roman shades that feature a thermal liner. Or, if you need total or near-total darkness (like in a bathroom or media room), Roman shades with a blackout liner may prove to be ideal.

Pleated Shades

Pleated shades are available with light-filtering and room-darkening liners, maximizing light control and privacy needs. With a light-filtering liner, pleated shades can deliver daytime light transmission indoors. To maximize privacy, use pleated shades with a privacy liner, so that only minimal shadows are visible from the outdoors.

On the other hand, a blackout liner offers maximum light obstruction. This liner may serve as a great selection in a child’s bedroom or other settings where complete darkness is needed.

Vertical Cellular Shades

Ready to take your vertical window treatments to the next level? Thanks to vertical cellular shades, you can block harsh sunlight from entering large windows and patio doors.

Vertical cellular shades have been shown to deliver year-round insulation, sound absorption and ultraviolet protection. Moreover, they can include blackout fabric to provide you with the total privacy you need to get a great night’s sleep. Keep in mind that the blackout fabric of vertical cellular shades features an opacity that prevents light from filtering through at all times.

Vertical cellular shades are ideal in climates with extreme hot and cold temperatures and can be specified to stack on either side, split down the middle or stack in the center for added convenience.

Examine your window treatment options closely, and you’re sure to find window shades that match your personal style and budget perfectly, while offering privacy from prying eyes.

Source: RisMedia

Sunrise Residences – Inviting & Contemporary New Rentals in Fairfield!

Discover the Enchantment….

This secret garden contains brand new studio and one bedroom units, modestly priced from $1475 – $1575. They are nestled among relaxing greenbelts within a quiet, gated community.

Our interiors include elevated ceilings, rich Euro-frame java beech wood cabinetry, stainless appliances, granite counters, microwave, washers/dryers and much more.

These inviting living spaces are convenient to shopping and commuter access. Lots of Bright Natural light, open floor plans, spacious baths, granite countertops and vanities, washer and dryer in every unit, mirrored wardrobes and lovely front patios. The gourmet kitchens are a chef’s delight! And don’t forget to take advantage of the wonderful community room for fun events. Located at 2750 North Texas Street in a secure gated community. Come on by and visit us for a tour or you can always call us at 707.421.9900.

|

|

|

|

|

|

|

|

|

|

|

|

5 Tips for First-Time Homebuyers

You’ve decided to go for it. You know mortgage rates are enticingly low. Buying a home can be thrilling and nerve-wracking at the same time, especially for first-time homebuyers. It’s difficult to know exactly what to expect.

Take these five steps to make the process go more smoothly.

Check Your Credit

Your credit score is among the most important factors when it comes to qualifying for a mortgage.

“In addition, the standards are higher in terms of what score you need and how it affects the cost of the loan,” says Mike Winesburg, formerly a mortgage planner in Wheeling, W. Va.

Scour your credit reports for mistakes, unpaid accounts or collection accounts.

Just because you pay everything on time every month doesn’t mean your credit is stellar. The amount of credit you’re using relative to your available credit limit, or your credit utilization ratio, can sink a credit score.

The lower the utilization rate, the higher your score will be. Ideally, first-time homebuyers would have a lot of credit available, with less than a third of it used.

Repairing damaged credit takes time. If you think your credit may need work, begin the repair process at least six months before shopping for a home.

Evaluate Assets and Liabilities

A first-time homebuyer should have a good idea of money they owe and money they have coming in.

“If I were a first-time homebuyer and I wanted to do everything right, I would probably try to track my spending for a couple of months to see where my money was going,” Winesburg says.

Additionally, buyers should have an idea of how lenders will view their income, and that requires becoming familiar with the basics of mortgage lending.

For instance, some professionals, such as the self-employed or straight-commission salesperson, may have a more difficult time getting a loan than others.

The self-employed or independent contractor will need a solid two years’ earnings history to show, according to Winesburg.

Organize Documents

When applying for mortgages, you must document income and taxes.

Typically, mortgage lenders will request two recent pay stubs, the previous two years’ W-2s, tax returns and the past two months of bank statements—every page, even the blank ones.

“Why it has to be every single last page, I don’t know. But that is what they want to see. I think they look for nonsufficient funds or odd money in or out,” says Floyd Walters, owner of a mortgage company in La Canada Flintridge, Calif.

Qualify Yourself

Ideally, you already know how much you can afford to spend before the mortgage lender tells you how much you qualify for.

By calculating debt-to-income ratio and factoring in a down payment, you will have a good idea of what you can afford, both upfront and monthly.

Though there’s not a fixed debt-to-income ratio that lenders require, the standard dictates that no more than 28 percent of your gross monthly income be devoted to housing costs. This percentage is called the front-end ratio.

The back-end ratio shows what portion of income covers all monthly debt obligations. Lenders prefer the back-end ratio to be 36 percent or less, but some borrowers get approved with back-end ratios of 45 percent or higher.

Figure Out Your Down Payment

It takes effort to scrape together the down payment.

There are programs that can assist buyers with qualifying incomes and situations.

“I’ve helped arrange assistance loans for $10,000, which are interest- and payment-free, and forgivable after five years. Although considered a loan, they’re more like grants. Other programs can provide up to $40,000 interest-free,” Winesburg says.

Finally, speak with mortgage lenders when you’re starting the process. Check with friends, co-workers and neighbors to find out which lenders they enjoyed working with and ask them questions about the process and what other steps first-time homebuyers should take.

Boost Curb Appeal in a Day…

Sometimes when planning to sell a house, in the name of renovating interior living spaces, updating bathrooms, replacing appliances and adding decorative touches throughout the bedrooms, homeowners leave outdoor curb appeal as a last priority. While of course the inside of a home is important, sellers make a big mistake when they neglect the exterior. Why is a home’s exterior so important? Consider this: Curb appeal is often a potential buyer’s first impression of a home, the very thing that helps him/her decide whether or not to come inside. Whether they’re shopping online or by cruising through neighborhoods, the outside of your property is the first thing they’ll notice. If you’re selling your home or about to, how can you quickly and effectively tackle the outdoor appeal? Here are some key tips for boosting the curb appeal in a way that means quick turnaround and increased home value:

1. Start with the Front Door. Believe it or not, your home’s front door can be one of its most important assets. A new steel entry door consistently ranks as one of the most rewarding projects in home repairs, yielding an increase in home value that’s greater than the costs to install one. Likewise, to make the door especially captivating, consider painting it a bold, pleasing color that will grab attention and add charm. When buyers see a new door that looks attractive, they see another asset that makes your home the one to buy.

2. Make Any Necessary Repairs. Is the driveway cracked or the front doorbell busted? Now is the time to call a repair company or get out your own toolbox to make repairs. Buyers want turnkey, move-in-properties, and that means they want properties with repairs already done. Do the work now to get your home in ship-shape condition.

3. Keep Up with Landscaping. From mowing the lawn to pulling weeds, make sure you’re keeping up with your outdoor landscaping so that your home looks presentable and well cared for at all times. Overgrown bushes and dying plants are a surefire signal to potential buyers that you’re not caring for your home and leaving more maintenance for them to handle.

4. Add Lighting. While most buyers will come visit your home during the daytime, it’s not at all unusual for the most interested ones to also drive by at night to see what nighttime curb appeal is like. Landscape lighting can make all the difference in terms of how a home looks, so make an investment in attractive lighting options that illuminate and add interest to your property. “Solar landscaping lights are a great addition to any yard because they don’t require complicated and expensive wiring,” says Bob Vila. “Remember, though, you get what you pay for—cheap lights won’t last as long and simply won’t look as good.”

5. Touch Up Paint. A fresh coat of paint is just as powerful outside as it is inside, so to update your home’s look, repaint the exterior or at least touch up problem areas. Another idea is to paint the trim a new color that creates either a nice complement or contrast to your home’s overall look.

6. Make Over the Mailbox. You might not think a mailbox matters much, but it’s yet another one of those little details that can add up together to make a strong impression on a buyer.

7. Add Outdoor Furniture. From rocking chairs on the front porch to an outdoor patio set on the back deck, outdoor furniture creates outdoor living spaces that expand your home’s appeal. Look for attractive, durable pieces that will endure weather damage and look good for years to come — whether or not you include these pieces with the home sale, setting them up is a great way to stage your home for greater resale value.

The bottom line when it comes to curb appeal is that a little investment today can add up to big rewards tomorrow. Take the time to update, clean, repair and add value to your property’s exterior now and you will make it more attractive to buyers, not to mention more beautiful to come home to. Use the tips above to get started now.

Source: Rismedia

Get Your Credit Score Ready for Homebuying Season!

Getting ready to buy a home this spring? Make sure there aren’t any cracks in your credit. A good credit score is essential when it comes to securing a mortgage.

“If (your score is) below 600, you’re probably not going to buy a home in the short term,” says Mike Sullivan, director of education at nonprofit credit and debt counseling agency Take Charge America.

Given the slew of stringent regulation introduced following the housing crisis, most lenders simply won’t risk extending this demographic credit. In fact, even consumers with good scores should polish up the ol’ credit report.

Qualifying for the best mortgage rates starts at a 740 credit score. Scores below that threshold will likely have higher interest on their home loans.

So if you plan on hitting up the housing market this April, make sure to pull a copy of your credit report and check to see where your score stands.

Check Your Status

Under the Credit Card Accountability Responsibility and Disclosure Act of 2009, or Credit CARD Act, everyone is entitled to one free credit report from each credit bureau every year.

Obtain a copy of this report from AnnualCreditReport.com. It won’t come with your score—you can purchase that for a nominal fee. But there also are websites that offer free versions of your score year-round.

A recent version of your credit report will show you where you stand in terms of creditworthiness. The report should also spell out what you need to do to improve your score.

“You don’t have to entirely guess,” Sullivan says. “You simply look at what (the score) takes into account and you deal with those issues.”

Get Current

You’ll definitely want to address any delinquent accounts on your record.

“If you are behind, you want to bring those up to date as soon as possible,” says Kathryn Moore, a certified consumer credit counselor with GreenPath Debt Solutions. Delinquent accounts are a huge red flag to mortgage lenders because they demonstrate a lack of ability to repay debts.

They’re also the quickest way to tank your credit score. A missed payment—particularly following an extended period of good credit behavior—can cause a drop of 70 to 90 points.

Sadly, you won’t immediately recoup all those points once the account is reported as up to date.

Instead, “you need to be patient and make all of your payments on time and slowly build your score up” again, says Stephen Brobeck, executive director of the Consumer Federation of America.

The role that time plays in building stellar credit is why it’s ideally “a good idea to look at your credit at least a year out” of shopping for a mortgage, says Bruce McClary, a spokesman for the National Foundation for Credit Counseling.

Getting a Quick Boost

If you are behind this timeline, there are a few steps you can take to potentially give your score a quick boost.

For starters, scan your credit report for accuracy. An error—such as an old, bad debt; incorrect account balance; or worse yet, a phantom foreclosure—could be needlessly weighing down your score. Have these errors corrected by contacting the credit bureau in question.

“There’s a link (on your credit report) to dispute any inaccurate information,” Moore says. “The credit bureau from there will have to resolve that dispute within 30 days.” Once a negative error is removed, your score should improve.

You can also engineer a quick boost by paying down existing debts, particularly high credit card balances. This move improves your credit utilization rate—essentially how much debt you are carrying versus how much credit has been extended to you — and should bolster your score.

Experts generally say to keep your credit utilization below 20 to 30 percent of your collective credit. However, “you really want to get that ratio down to rock bottom if you’re looking for a house,” McClary says.

Clearing out existing balances will also improve your debt-to-income ratio, which a “lender looks at” closely during their mortgage decision process, Moore says.

Lenders typically say the “back-end” debt-to-income ratio—or the amount of your income that is needed to cover all your monthly debt obligations, including credit card bills and other loans—should be 36 percent or lower.

Finally, if you recently missed a loan payment because you, say, didn’t know about the bill, try calling up the issuer (or lender) to see if they will refrain from letting the credit bureaus know about your faux pas.

What to Avoid

Once you have your score in the upper echelon, make sure it stays there. Avoid running up your credit card balances again, which will help keep your credit utilization in check.

Also avoid applying for other loans, including store credit cards, particularly in an attempt to improve this aforementioned credit utilization rate. Applying for new credit generates hard inquiries on your credit report, which could ding your score.

And “if those inquiries don’t necessarily show up as approved accounts, that sends up a red flag” to lenders because it could look like you were turned down for a credit line, McClary says.

Not to mention that you’re more likely to miss a payment when you have multiple cards at your disposal, Brobeck says.

Conversely, don’t close any accounts while you are looking for a mortgage, as the closure could send your credit utilization skyrocketing in the wrong direction.

Source: RisMedia/Bankrate.com

MUST DO’s Before you move into your new home!

The moving frenzy never ends: Even after you close, the to-do lists drag on and on—endless pages of bullet points that keep you up at night when all you want is to begin your new life. Some of them are fun, like redecorating and buying new furniture.

“When you move into a new house, you’re more concerned with decorating and taking stuff out you don’t like,” says Kevin Minto, president of Signet Home Inspections in Grass Valley, CA. “But let’s not forget about the less romantic things that are mundane—but more important in the long run.”

Once you’ve got the keys, feel free to give yourself a break. You deserve it! But don’t rest on your laurels too long—and make sure to do these eight things right away.

1. Change the locks

Before moving even one tiny piece of furniture into your new home, change the locks—or at least have them rekeyed. It’s not that you don’t trust the sellers (who are, we’re sure, perfectly respectable and upstanding citizens). It’s that you shouldn’t trust everyone who’s had contact with those keys over the years, any of whom could have copied the keys for some unsavory purpose.

2. Change the alarm batteries

Making sure your fire and carbon monoxide detectors have fresh batteries may not seemlike a pressing issue while you’re in the middle of a stressful move (and aren’t they all), but it’s the kind of thing that gets ignored and then forgotten. Better to deal with it now, when the home is empty and you can make a quick sweep of the house—without lugging a ladder around furniture.

3. Review your home inspector’s report

Can’t find your inspector’s report? Minto says reports are often filed with the escrow papers—but don’t wait until something goes wrong to pull them out. A good home inspector will outline the most important issues in their report, so use their expertise as a guide for your first few days of ownership. If they’ve marked anything as particularly pressing, make sure to handle it before moving in.

4. Find the circuit breaker

If you were there during inspection, you should know where your junction box is, but if you don’t, finding it “should be the first and foremost thing that should be attended to,” Minto says. During a move, when you’re plugging all sorts of electrical doodads into the wall, you don’t want to be lost in the dark hunting for that elusive metal box. (While you’re there, find the water shut-off, too.)

Then, get familiar: If it’s not already well-marked, have your spouse or another family member stand in different parts of the house while you flip different switches, and make a note of which ones handle different rooms.

5. Deal with any water problems

Looking at that inspector’s report? Deal with water-related issues immediately, says Minto. These tend to be troublesome because they’re so easily ignored—”out of sight, out of mind,” he says. A leaky toilet might seem minor, but the steady drip can damage internal structural components.

Check your roof, too: If the rubber vent boots on your roof are leaking, you might not know it for a while.

“By the time they see it in a ceiling, there’s been a fair amount of water,” Minto says.

6. Caulk everything

This one isn’t mandatory, but caulking is a whole lot easier if you do it when the house is empty, letting you see all the nooks and crannies that might need a little sealing—and don’t forget the exterior. Minto says he sees caulking issues on “every home,” and while they might seem minor, it doesn’t take long before cracking gives way to leaks and even more water issues.

7. Plan your emergency exits

Before you begin bringing in furniture, walk through every room and decide how you would escape in an emergency. This can help

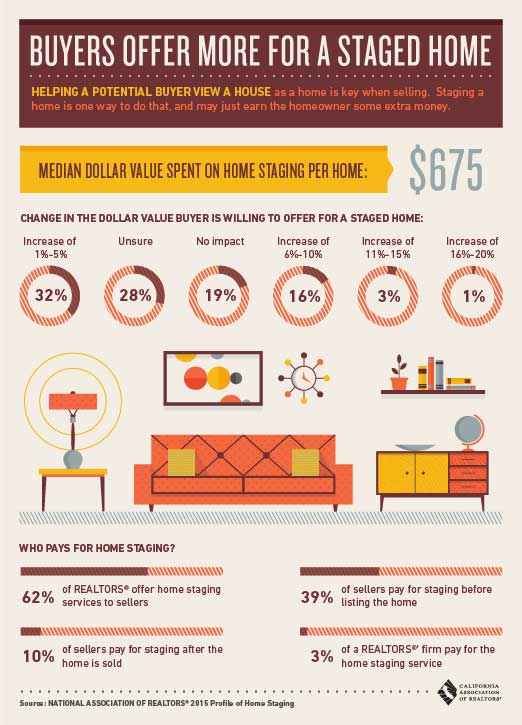

Buyers Offer More for a Staged Home

The Effect of Environmental Hazards on Home Value

There are several factors that weigh on home value, including condition, location, and—in areas where they are most pronounced—environmental hazards such as poor air quality.

According to the ATTOM Data Solutions recent Environmental Hazards Housing Risk Index, 17.3 million single-family homes and condominiums have a high risk of an environmental hazard, with Denver, Colo., San Bernardino, Calif., and Curtis Bay, Md., facing the highest risk. Environmental hazards include brownfields, or property contaminated (or potentially contaminated) by a hazardous substance, polluters, poor air quality and superfunds.

“Home values are higher and long-term home price appreciation is stronger in zip codes without a high risk for any of the four environmental hazards analyzed,” says Daren Blomquist, senior vice president at ATTOM Data Solutions. “Corresponding to that is a higher share of homes still seriously underwater in the zip codes with a high risk of at least one environmental hazard, indicating those areas have not regained as much of the home value lost during the downturn.

“Conversely, home price appreciation over the past five years was actually stronger in the higher-risk zip codes, which could reflect the strong influence of investors during this recent housing recovery,” Blomquist says. “Environmental hazards likely impact owner-occupants more directly than investors, making the latter more willing to purchase in higher-risk areas. The higher share of cash sales we’re seeing in high-risk zip codes for environmental hazards also suggests that this is the case.”

In areas with a “very high” brownfield risk, 17.2 percent of properties are “seriously underwater,” according to the Index; in areas with a “very low” brownfield risk, 8.9 percent of properties are seriously underwater. Median home prices in very high brownfield risk areas are 2.8 percent below 10 years prior, while median home prices in very low brownfield risk areas are 2.8 percent above 10 years prior. Home sellers in very high brownfield risk areas gained 25.3 percent on average at sale, while sellers in very low brownfield risk areas gained 18.9 percent.

In areas with a very high polluter risk, 12.7 percent of properties are seriously underwater, compared to 9.2 percent of properties seriously underwater in very low polluter risk areas. Home sellers in very high polluter risk areas gained 16.6 percent on average at sale, while sellers in very low polluter risk areas gained 27.7 percent.

For areas with a “low” or “moderate” risk of poor air quality, home sales volume has increased 26 percent in the past five years, according to the report; for areas with a “high” risk of poor air quality, home sales volume has increased 16.5 percent in the past five years, while in areas with a very high risk of poor air quality, home sales volume has increased 3.3 percent over the past five years.

Median home prices in very high superfund risk areas are 1.5 percent below 10 years prior. Home sellers in high superfund risk areas gained 19.6 percent on average at sale, while sellers in very low superfund risk areas gained 24.4 percent.

Source: Rismedia

")