Facebook

Facebook

Twitter

Twitter

Pinterest

Pinterest

Copy Link

Copy Link

MUST DO’s Before you move into your new home!

The moving frenzy never ends: Even after you close, the to-do lists drag on and on—endless pages of bullet points that keep you up at night when all you want is to begin your new life. Some of them are fun, like redecorating and buying new furniture.

“When you move into a new house, you’re more concerned with decorating and taking stuff out you don’t like,” says Kevin Minto, president of Signet Home Inspections in Grass Valley, CA. “But let’s not forget about the less romantic things that are mundane—but more important in the long run.”

Once you’ve got the keys, feel free to give yourself a break. You deserve it! But don’t rest on your laurels too long—and make sure to do these eight things right away.

1. Change the locks

Before moving even one tiny piece of furniture into your new home, change the locks—or at least have them rekeyed. It’s not that you don’t trust the sellers (who are, we’re sure, perfectly respectable and upstanding citizens). It’s that you shouldn’t trust everyone who’s had contact with those keys over the years, any of whom could have copied the keys for some unsavory purpose.

2. Change the alarm batteries

Making sure your fire and carbon monoxide detectors have fresh batteries may not seemlike a pressing issue while you’re in the middle of a stressful move (and aren’t they all), but it’s the kind of thing that gets ignored and then forgotten. Better to deal with it now, when the home is empty and you can make a quick sweep of the house—without lugging a ladder around furniture.

3. Review your home inspector’s report

Can’t find your inspector’s report? Minto says reports are often filed with the escrow papers—but don’t wait until something goes wrong to pull them out. A good home inspector will outline the most important issues in their report, so use their expertise as a guide for your first few days of ownership. If they’ve marked anything as particularly pressing, make sure to handle it before moving in.

4. Find the circuit breaker

If you were there during inspection, you should know where your junction box is, but if you don’t, finding it “should be the first and foremost thing that should be attended to,” Minto says. During a move, when you’re plugging all sorts of electrical doodads into the wall, you don’t want to be lost in the dark hunting for that elusive metal box. (While you’re there, find the water shut-off, too.)

Then, get familiar: If it’s not already well-marked, have your spouse or another family member stand in different parts of the house while you flip different switches, and make a note of which ones handle different rooms.

5. Deal with any water problems

Looking at that inspector’s report? Deal with water-related issues immediately, says Minto. These tend to be troublesome because they’re so easily ignored—”out of sight, out of mind,” he says. A leaky toilet might seem minor, but the steady drip can damage internal structural components.

Check your roof, too: If the rubber vent boots on your roof are leaking, you might not know it for a while.

“By the time they see it in a ceiling, there’s been a fair amount of water,” Minto says.

6. Caulk everything

This one isn’t mandatory, but caulking is a whole lot easier if you do it when the house is empty, letting you see all the nooks and crannies that might need a little sealing—and don’t forget the exterior. Minto says he sees caulking issues on “every home,” and while they might seem minor, it doesn’t take long before cracking gives way to leaks and even more water issues.

7. Plan your emergency exits

Before you begin bringing in furniture, walk through every room and decide how you would escape in an emergency. This can help

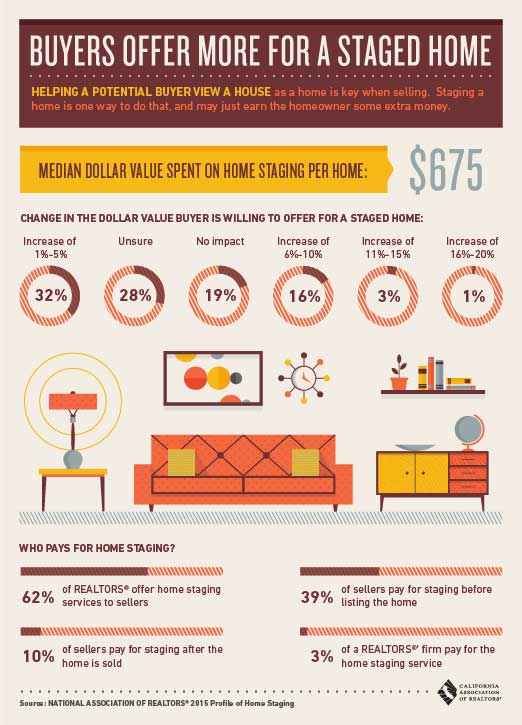

Buyers Offer More for a Staged Home

The Effect of Environmental Hazards on Home Value

There are several factors that weigh on home value, including condition, location, and—in areas where they are most pronounced—environmental hazards such as poor air quality.

According to the ATTOM Data Solutions recent Environmental Hazards Housing Risk Index, 17.3 million single-family homes and condominiums have a high risk of an environmental hazard, with Denver, Colo., San Bernardino, Calif., and Curtis Bay, Md., facing the highest risk. Environmental hazards include brownfields, or property contaminated (or potentially contaminated) by a hazardous substance, polluters, poor air quality and superfunds.

“Home values are higher and long-term home price appreciation is stronger in zip codes without a high risk for any of the four environmental hazards analyzed,” says Daren Blomquist, senior vice president at ATTOM Data Solutions. “Corresponding to that is a higher share of homes still seriously underwater in the zip codes with a high risk of at least one environmental hazard, indicating those areas have not regained as much of the home value lost during the downturn.

“Conversely, home price appreciation over the past five years was actually stronger in the higher-risk zip codes, which could reflect the strong influence of investors during this recent housing recovery,” Blomquist says. “Environmental hazards likely impact owner-occupants more directly than investors, making the latter more willing to purchase in higher-risk areas. The higher share of cash sales we’re seeing in high-risk zip codes for environmental hazards also suggests that this is the case.”

In areas with a “very high” brownfield risk, 17.2 percent of properties are “seriously underwater,” according to the Index; in areas with a “very low” brownfield risk, 8.9 percent of properties are seriously underwater. Median home prices in very high brownfield risk areas are 2.8 percent below 10 years prior, while median home prices in very low brownfield risk areas are 2.8 percent above 10 years prior. Home sellers in very high brownfield risk areas gained 25.3 percent on average at sale, while sellers in very low brownfield risk areas gained 18.9 percent.

In areas with a very high polluter risk, 12.7 percent of properties are seriously underwater, compared to 9.2 percent of properties seriously underwater in very low polluter risk areas. Home sellers in very high polluter risk areas gained 16.6 percent on average at sale, while sellers in very low polluter risk areas gained 27.7 percent.

For areas with a “low” or “moderate” risk of poor air quality, home sales volume has increased 26 percent in the past five years, according to the report; for areas with a “high” risk of poor air quality, home sales volume has increased 16.5 percent in the past five years, while in areas with a very high risk of poor air quality, home sales volume has increased 3.3 percent over the past five years.

Median home prices in very high superfund risk areas are 1.5 percent below 10 years prior. Home sellers in high superfund risk areas gained 19.6 percent on average at sale, while sellers in very low superfund risk areas gained 24.4 percent.

Source: Rismedia

What You Need to Know Before Buying Mortgage Insurance

If you’re like many borrowers who have less than 20 percent of a home’s value in equity or saved for a down payment, you need to know how mortgage insurance affects the cost of buying a home.

What Is Mortgage Insurance?

Mortgage insurance—also known as private mortgage insurance, or PMI—protects lenders from default on conventional mortgages in cases in which the borrower contributes a down payment of less than 20 percent of the home’s purchase price. PMI is different from homeowners insurance, which protects the home and what’s in it. It’s also different from mortgage protection insurance or mortgage life insurance, which is an insurance policy that pays off the mortgage loan if the borrower passes away. Mortgage insurance is beneficial to both lenders and borrowers. Mortgage insurance lowers a lender’s risk of giving a loan to borrowers with a low down payment. It also benefits the borrower, who, with mortgage insurance, might now qualify for a mortgage he wouldn’t otherwise get approved for.

What You’ll Pay for Mortgage Insurance

The cost of mortgage insurance depends on the type of home loan you have. You could pay anywhere from 0.3 percent to 1.15 percent of your home loan, according to realtor.com®.

Although insurance premium payments usually get paid monthly, you might have the option to pay it up front at closing or roll it into the home loan cost. Check with your lender.

Mortgage Insurance for Different Types of Home Loans

Mortgage insurance programs vary depending on the type of home loan. Generally, mortgage insurance is required when you get a conventional mortgage and put down less than 20 percent, or when you refinance a mortgage and your home equity is less than 20 percent.

Other types of mortgage insurance include:

- Federal Housing Administration mortgage insurance (mortgage insurance premium): An MIP is required for all FHA loans. All borrowers pay their mortgage premiums directly to the FHA, and premiums are the same for everyone regardless of credit score—though if your down payment is less than 5 percent, you can expect to pay a little more. If you get an FHA loan, budget for both monthly MIP costs as part of your regular payment and an upfront payment included in your closing costs. FHA mortgage insurance rates are usually about 0.625 percent.

- U.S. Department of Agriculture home loan insurance: U.S. Department of Agriculture insurance covers USDA home loans. It’s a lot like FHA mortgage insurance but less expensive. USDA home loan insurance requires making a payment both at closing and as part of your monthly payments. You have the option to roll the upfront cost into your mortgage, but if you do this, you’ll increase both your monthly payment and your overall loan cost.

- VA home loan guarantee: VA loans come with a mortgage guarantee instead of mortgage insurance, but it provides similar benefits. Instead of a monthly mortgage insurance premium, you’ll pay a funding fee upfront. The fee amount varies depending on factors like your military service type, down payment amount, disability eligibility, whether you are purchasing or refinancing, and if you’ve had a previous VA loan.

Alternatives to Mortgage Insurance

Although there are benefits to mortgage insurance, having it adds to the cost of getting a home loan. If you want to cut costs or are ready to get rid of PMI, consider these five alternatives to mortgage insurance.

Pay a higher interest rate.

When financing a home, some lenders might offer the option to avoid PMI by accepting a higher interest rate. If you choose this option, the higher mortgage rate cannot get canceled, so you’ll have to refinance to lower your rate in the future.

Get your home reappraised.

If you believe you now have at least 20 percent equity in your home due to renovations or the rising local property values, get your home reappraised. You might have enough equity to cancel your mortgage insurance, but you’ll have to pay for the appraisal up front.

Get a piggyback loan.

Whether your lender calls them piggyback loans or piggyback mortgages, these home equity loans or credit lines enable borrowers with low down payments to borrow more money. Before applying or signing for one, review the fine print carefully to see if your total monthly cost is actually cheaper than paying for mortgage insurance.

Ask your lender about other programs.

Some lenders offer programs that don’t require mortgage insurance, even with down payments below 20 percent, though you’ll likely have to prove that you have excellent credit to qualify. Before talking to your lender, focus on building your credit history, especially if you or your spouse has bad credit.

Save more for a down payment.

Sometimes it pays to wait and save up or to choose a home that requires a down payment you can afford. If you save 20 percent of the home’s purchase price to use as a down payment, you might qualify for a conventional mortgage without mortgage insurance. A conventional loan comes with a lower interest rate, and you’ll be able to avoid the headache of comparing mortgage insurance rates altogether.

Source: Rismedia

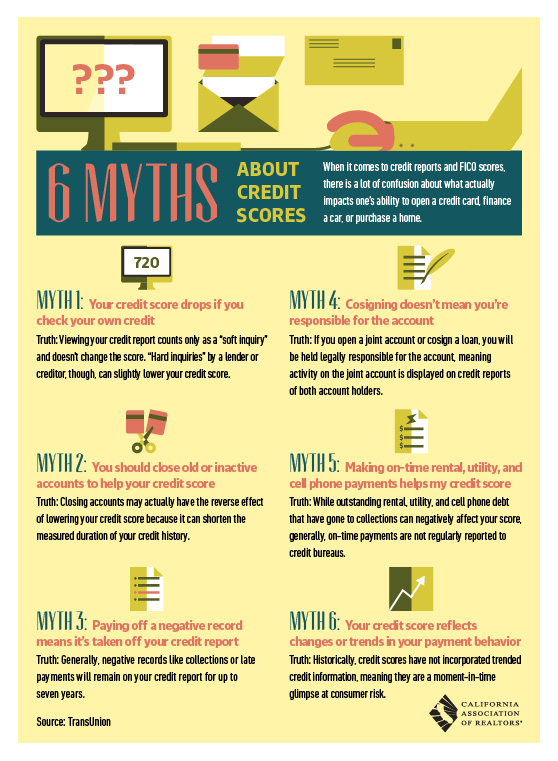

6 Myths about Credit Scores

7 Ways Home Sellers Turn off Homebuyers

When it’s time to sell your home, you can invest a ton of time, energy and money into getting the place ready for sale. You might declutter, stage and even remodel the house to make it as appealing to buyers as possible.

Sometimes, though, no amount of preparation can overcome something in the home that, rightly or wrongly, offends some buyers and gives them negative impressions of you and your house. These potentially troublesome items create a dilemma for real estate agents, says Maura Neill, a REALTOR® in Alpharetta, Ga.

“We tell our seller clients to depersonalize a house,” Neill explains. “You want buyers to feel as though they could make themselves at home, move in and be comfortable.”

The risk of ignoring the agent’s advice is considerable. Buyers “may turn around and leave,” Neill says. With that in mind, here are seven things that might offend buyers and result in fewer offers.

Live Animals

Believe it or not, some sellers keep live, unclean and potentially dangerous animals in homes for sale.

Wendy English, a former real estate sales manager in Medfield, Mass., recalls an uncaged rabbit that she says was “disgustingly smelly” and would chase people and try to bite them when they entered the home. “The homeowner just loved the rabbit, didn’t see any problems with it, thought it was the cutest pet ever and was maybe immune to the smell,” English says. “The rabbit was definitely horrible.”

Courtney Self, a broker/owner in Torrance, Calif., experienced what might have been an even worse situation. “I had a listing with monkeys that flung their feces when we would show the house,” she says.

Animal-Head Trophies

Dead animals also can be problematic.

Barry Bevis, a broker/owner in Tallahassee, Fla., recalls a for-sale home that had a “trophy” room over the garage. “The pictures of the house (online) had these giant elk heads and deer heads,” he says. “It’s better to leave it out. You’re going to offend too many people.”

By the way, not everyone loves pets either, so food bowls, litter boxes, play toys and the like should be removed from a home when it’s on the market, Bevis says. “Many people are allergic to animals or feel like the animals cause too much wear and tear,” he explains. “If you have any evidence of pets in your property, it’s going to turn off a large segment of buyers.”

Flags

“You never expect to see a Nazi flag hanging on the wall,” says Neill, “but we walked into a seemingly vanilla suburban house and into what appeared to be a teenager’s bedroom and there was a giant flag with a swastika on it hanging on the wall.”

Indeed, any sort of emotionally charged or polarizing display like, say, a Confederate flag, can also be offensive. “There’s a debate about whether it’s heritage and pride or racism and bigotry,” Neill says. “Depending on who you talk to, you get a different answer.”

Bevis recalls an incident when such a flag created a negative impression. “I was showing a house to an African-American couple,” he says. “I opened the lockbox and the key was (stamped with) a Confederate battle flag. It really did turn these folks off just a little bit. Immediately they didn’t like the people selling the house.”

Sports Memorabilia

Sports team rivalries fuel strong emotions, and a seller’s spirted support of the “wrong” team can create a sour impression.

“Having your house decked out in your team might not offend buyers, but it will color the way they think about that house,” Neill says. “It’s usually not (just the owner’s) team’s stuff. It’s also stuff making fun of their rivals. Buyers don’t want to walk into a house that’s berating their team.”

English says long-distance relocating buyers (known as “relos”) are most likely to be put off. “Relos will come in and see Patriots stuff, Red Sox stuff, and it does rub them the wrong way,” she says. “Sellers don’t necessarily realize how strongly someone might react to their favorite team.”

Nudity

Whether it’s baby pictures, artwork or pornography, nudity makes some buyers uncomfortable. In some cases, sellers don’t realize they’ve exposed too much information. In others, sellers want to make a statement, even if it’s at their own expense.

“Anybody who has a tasteful painting usually will get the reasoning that it makes sense to take it down,” says English. “The not-tasteful stuff, I think those people are going for the shock value, which doesn’t help sell the house.” Self offers a few examples of things she’s seen in for-sale homes: a statue of male genitalia next to a bed, wallpaper patterned with nude women in a guest bathroom and a drunk heir (yes, a live person), shirtless and passed out on the floor.

Mystery Rooms

When buyers want to see a for-sale house, they expect to see the whole house, not just parts of it. That makes a locked room a big turnoff, English says. Whatever’s behind the door might be innocuous, but buyers have no way to know for sure as long as they’re kept out.

“Every so often there will be a house where the homeowner will have a locked room that you can’t see and that always makes buyers say, ‘Forget it,'” English says.

Mysterious objects can trigger a similar reaction. English recalls a home that had a very large rock covered with plywood boards in the basement. “Part of the home inspection was that the buyer wanted to remove the plywood and see what was underneath it. It was just a rock, as the seller had said, but everyone called it ‘the coffin,'” she says.

Drugs

Despite relaxed laws in some states, marijuana and other drugs are still federally illegal and their presence or evidence of use, including odors, in a home can deter buyers. Derek Turner, a broker/owner in Ventura, Calif., says he encountered an empty beer can wall and marijuana paraphernalia on a coffee table and kitchen counter in a for-sale home. Turner says, “My client did not write an offer.”

Source: RisMedia

Smart Home Resources

The ABCs of Smart Home Technology

Don’t know where to start with smart home technology and devices? We’ve compiled an A-to-Z dictionary to help guide you to pro status.

What’s in a Name? Defining the Smart Home

What’s in a Name? Defining the Smart Home

As smart home technology enters the mainstream, both sales associates and consumers have asked themselves what truly constitutes a home that is smart. Coldwell Banker and CNET have joined forces to put the debate to rest and truly define the modern Smart Home.

What is a Smart Home?

What is a Smart Home?

In this segment of NBC Open House, Coldwell Banker Real Estate and CNET.com establish a definition for the “smart home” that is simple while allowing still for choices.

Smart Home Security: Where to Start

Smart Home Security: Where to Start

In the second post of the Smart Home Security series, we explore where homeowners can begin when looking to enhance their home security using smart home technology and devices.

The 2017 Smart Home Marketplace Survey

The 2017 Smart Home Marketplace Survey

Coldwell Banker teamed up with Vivint Smart Home ahead of this year’s Consumer Electronics Show (CES) to see what consumers were looking for in smart home technology. Turns out, Americans are ready to have a voice-enabled home.

How the Internet of Things is Changing a Little Place Called Home

How the Internet of Things is Changing a Little Place Called Home

How IoT is changing the business of real estate.

Smart Home Technology: 7 Surprising Features

Smart Home Technology: 7 Surprising Features

Lights, cams, doors, security — many homeowners know the basics about home automation and smart home technology. But there’s a whole array of fun smart home features that you’ve never dreamed of, from watering plants to feeding pets.

8 Ways to Outsmart the Weather In A Smart Home

8 Ways to Outsmart the Weather In A Smart Home

Do more to combat and prepare for the weather–rain, shine, snow–than you thought possible.

3 Smart Home Devices to Help with Storm Preparation

3 Smart Home Devices to Help with Storm Preparation

There are a number of smart home technologies that make storm preparation and damage prevention easier than ever.

")